Research

Marching Backwards

The emerging pro-defendant class action landscape.

Statistical measures of fund performance can support investors’ decisions by providing a clearer picture of the fund manager’s performance against the fund benchmark over a period of time. The number of index tracking Exchange Traded Funds (ETFs) is constantly growing, providing an overwhelming number of options for investors. The ability to discriminate between good managers (those who add real value) from bad managers (those who do not generate any alpha) is an important step towards greater investor awareness.

On 2 February 2016, the European Securities and Markets Authority (ESMA) issued a statement highlighting the issue of closet index tracking funds. In it they described the analysis ESMA had undertaken to “determine whether any indication of closet indexing can be found at an EU-wide level”.

ESMA’s study looked at the universe of European UCITS funds. The metrics used to analyze these funds were Active Share1, Tracking Error2 and R-Squared3. Based on these metrics, ESMA stated that between 5 – 15% of European UCITS funds could be classified as potential closet indexers4.

Fideres has conducted a similar review of the European fund market for European NGO Better Finance (the European Federation of Investors and Financial Services Users)5. Like ESMA, Fideres used the Morningstar database for their research. The results are based on publicly available information published by ESMA and Fideres’s market research.

Fideres filtered the universe of all managed funds using the following criteria:

The resulting sample was composed of 2,333 funds. Further filtering removed funds which did not have available data during the period of 2010 – 2014 (inclusive). Due to unavailable data, more than 56% of the original sample was filtered out. The thresholds used by ESMA to classify funds were then applied to the final sub-sample of 1014 funds as follows:

European Closet Indexers: 3 Shades Of Grey_T1

Classification

Threshold

for at least 3 of the 5 years analysed

Active

Share

Tracking Error

R-Squared

Classification

1

<60%

<4%

n/a

Classification

2

<50%

<3%

n/a

Classification

3

<50%

<3%

>95%

Fideres’s results align closely to ESMA’s results. The decrease in the number of funds in the sample may be explained by a change in the number of available funds. This could be due to the closure of some funds, during the time period between the conclusion of ESMA’s and Fideres’s studies.

| Results Table | Sample Size | Sub-Sample (Filtered for data availability) | Classification 1 | Classification 2 | Classification 3 |

| Fideres' Study | 2333 | 1014 | Funds: 166 | Funds: 67 | Funds: 63 |

| Proportion: 16% | Proportion: 7% | Proportion: 6% | |||

| ESMA's Study | 2600 | 1251 | Funds: 188 | Funds: 88 | Funds: 63 |

| Proportion: 15% | Proportion: 7% | Proportion: 5% |

Approximately 25% of the sub-sample funds had an active share of less than 60%, the level often quoted in academic literature as being a potential boundary between active and passive funds.

The sub-sample group represents all eligible supposedly actively managed funds. By applying the metric thresholds, the Classification groups will naturally have a lower Active Share and Tracking Error and higher R-squared. Summary statistics of the sub-sample and Classification groups are shown below:

| Number of Funds | AS | TE | R-Squared | Management Fee Starting | Fund Size (EUR) | |

| Sub-sample | 1014 | 71.24% | 4.68% | 91.33% | 1.49% | 586,232,604 |

| Classification 1 | 166 | 43.25% | 2.80% | 96.49% | 1.48% | 400,119,115 |

| Classification 2 | 67 | 35.95% | 2.12% | 98.14% | 1.46% | 272,966,085 |

| Classification 3 | 63 | 35.69% | 2.05% | 98.33% | 1.47% | 272,153,044 |

An interesting result of Fideres’s study is that the management fees charged by the funds in the Classification groups are in line with the sub-sample group. This reinforces the notion that potential closet index funds may be tracking a benchmark, but are still charging management fees in line with an actively managed fund.

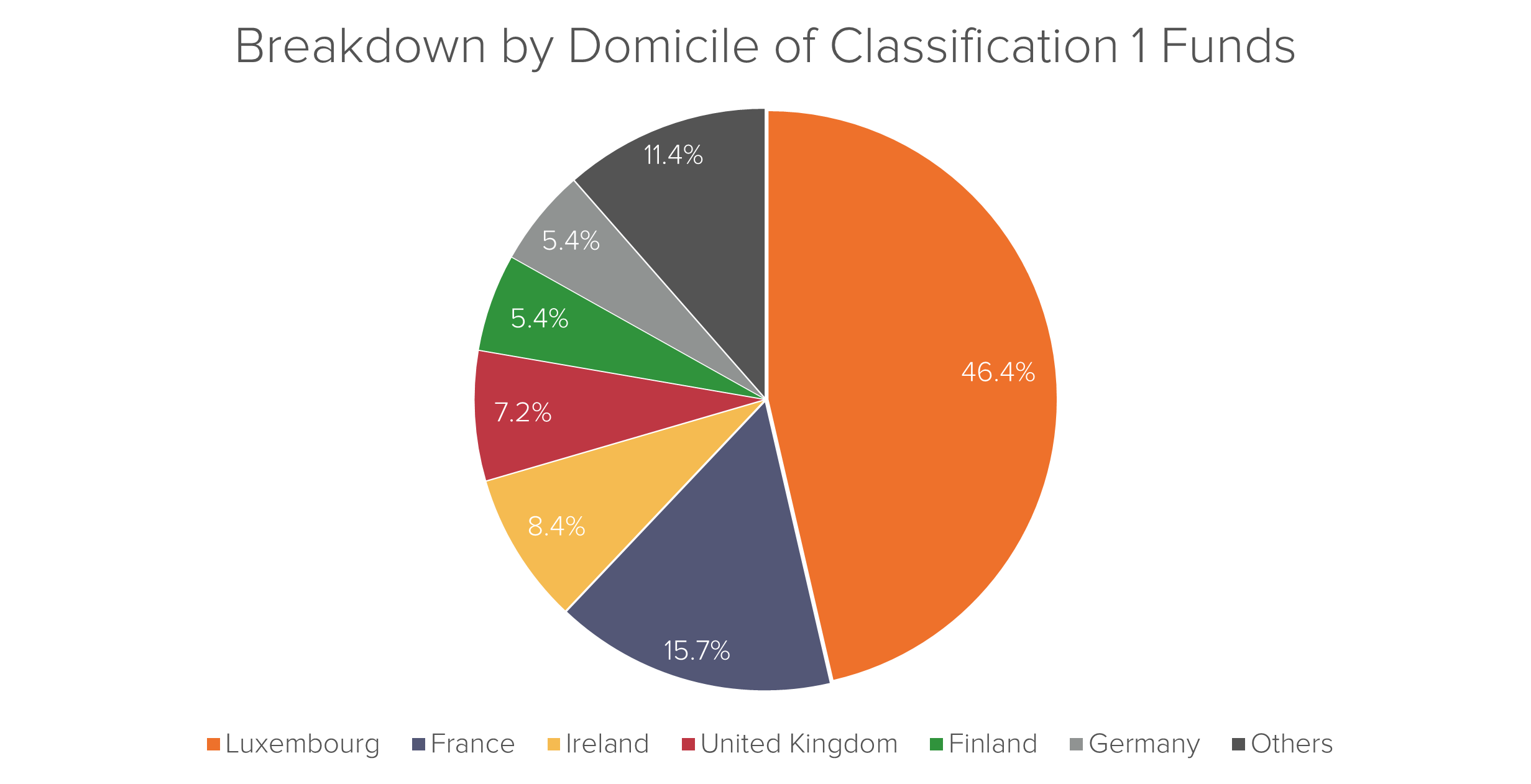

Earlier this month, a Financial Times article stated that the French regulator concluded “that no French asset manager is offering so-called closet trackers — funds that follow an index closely but charge high fees for active management”7 However, Fideres’s study suggests that approx. 15.7% of the Classification 1 funds are domiciled in France.

In July 2016, in response to ESMA’s work on closet indexers, the European Fund and Asset Management Association (EFAMA) published a report which partly criticized ESMA’s study stating that “a wide range of factors must be taken into account to assess whether a fund is being actively managed”8.

Fideres agrees that many academic papers and the ESMA study itself put too much emphasis on active share and tracking error. These are useful but not sufficient. In order to identify whether a fund is a potential closet indexer, one needs to look beyond simply the active share, tracking error and R-squared.

As we have mentioned in our previous research alert, Closet Indexers Hiding Behind a High Active Share, relying solely on these metrics can be deceiving. To understand the full scope of closet indexing requires determining whether the management of the fund is consistent with the stated investment strategy. Legal analysis is needed to identify misleading statements made in the prospectus, combined with the quantitative analysis of fund performance.

1 Active share represents the proportion of portfolio holdings that differ from those in the benchmark index

2 Tracking error is a measure of the volatility of excess returns relative to a benchmark

3 R-Squared reflects the percentage of a portfolio’s movements that can be explained by movements in its benchmark

6 Fund size in base currency

7 https://www.ft.com/content/9674ce96-d743-11e6-944b-e7eb37a6aa8e

8 https://fideres.com/wp-content/uploads/2023/02/6-July-2016-EFAMA_Report-on-Closet-Index-Funds.pdf

Russell joined Fideres in 2014. He has acted as a consulting expert in many large legal cases in the US and UK for a variety of industries. In particular, he leads the pharmaceutical antitrust team in relation to generic drug price-fixing allegations, labour economics team in relation to wage suppression and has carried out expert work in financial markets claims involving swap mis-selling and fund management excess fees. Russell is a Chartered Financial Analyst (CFA) charter holder and completed his BSc in Accounting and Finance at the London School of Economics and Political Science.

The emerging pro-defendant class action landscape.

Fideres analyses the potential impact of Covid-19 on the CLO market.

Fines for Standard & Poor’s are too little, too late.

London: +44 20 3397 5160

New York: +1 646 992 8510

Rome: +39 06 8587 0405

Frankfurt: +49 61 7491 63000

Johannesburg: +27 11 568 9611

Madrid: +34 919 494 330