Key Points

- European Commission decisions of 2016 and 2017 found six European truck manufacturers guilty of price-fixing for a 14-year period.

- To assist with follow-on claims, Fideres has built a preliminary damages model, which estimates the overcharge on direct purchases as well as on interest payments for truck lease agreements.

- Fideres has access to a dataset of historical truck prices by make, model and all possible configuration options, from 1990 to 2017, which enables us to estimate the overcharge on any truck purchased during the cartel period.

Outline Damage Analysis

The damages analysis comprises three key steps:

- Calculate but-for prices, i.e. the prices which would have prevailed in the absence of the cartel;

- Estimate damages, i.e. the overcharge paid on trucks purchased by the claimants and inflated payments on leases or other contractual arrangements, where applicable;

- Estimate pass-through of damages, where relevant.

Historical Prices

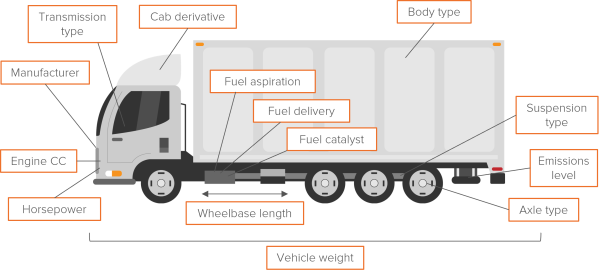

As outlined above, the damages analysis requires the calculation of but-for prices. Fideres has obtained access to a highly granular database of historical trucks prices which will allow us to calibrate the but-for pricing model. The data is broken down by the following specifications:

The dataset covers the period 1990 to 2017 and contains 30,200 historic Cost New Prices across over 3,000 distinct new Heavy Commercial Vehicle models in the over 6 tonne category. The major benefit of this dataset is that it includes a significant amount of pre- and post-cartel period data. The trucks cartel was in effect for the years 1997 to 2011. This means that we have seven years of pre-cartel prices and 6 years of post-cartel prices against which we can compare the observed and modelled cartel-period prices.

The high level of detail in the dataset not only allows us to model statistically robust but-for prices, but also enables us to calculate highly specific damages estimates which can be applied directly to the claimant’s exact fleet.

But-For Price Analysis

Using historical prices and truck specification data, we can estimate the effect of the cartel on the price of any truck. Regression analysis allows us to express the observed price (P) as a function of a number of factors which would affect price, such as the manufacturer, engine size, the costs of production, including a variable to indicate the years of the cartel, as follows:

P = α + β1 Engine_Size + β2_Manufacturer + … + β3_Production_Cost + β4_Cartel_Period + ε

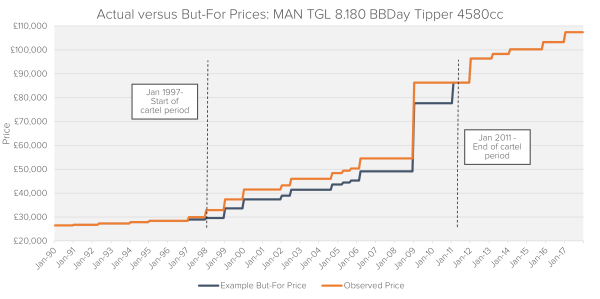

Using the regression above, it is possible to estimate the impact of the cartel on the price of trucks during the cartel period. The effect of the cartel is then subtracted from the observed price in order to determine the but-for price. In the illustrative chart below, the difference between the actual price (in red) and the but-for price (in blue) represents the price effect of the cartel.

Damages Estimation

Damages can be direct (outright purchases) or indirect (e.g. leases). For outright purchases, the but-for price is subtracted from the actual price of each individual truck in the claimant’s fleet at the time that it was purchased in order to obtain a total overcharge. Direct damages are then calculated as the overcharge on each truck, multiplied by quantity purchased.

In the case of indirect purchases – e.g. financial lease, hire purchase or operational lease arrangements – interest and other payments are higher than they would have been since they are based on an inflated notional amount. Using the estimated but-for prices, each component of the lease payment can be recalculated based on this new, lower notional. Indirect damages are therefore the difference between the sum of original lease payments and the sum of lease payments based on the but-for price, multiplied by the number of lease agreements entered into. It is also possible that the claimant may have passed on some of the price increases to their own customers downstream. In this case, the extent of the pass-though can be calculated using regression analysis and subtracted from the final damages analysis.