Key Points

- Deutsche Bank’s fine of £226.8 million is highest yet in the LIBOR scandal.

- FCA’s report on LIBOR manipulation lacks any quantitative analysis.

- Fideres estimates that LIBOR manipulation continued beyond the period covered by the FCA investigation.

Update

On April 23, 2015, the UK’s Financial Conduct Authority (“FCA”) fined Deutsche Bank GBP 226.8 million for its role in manipulating LIBOR, the largest fine it has issued to date in respect of LIBOR manipulation. In this research alert, Fideres gives an overview of the industry-wide LIBOR fines and their implication for private lawsuits.

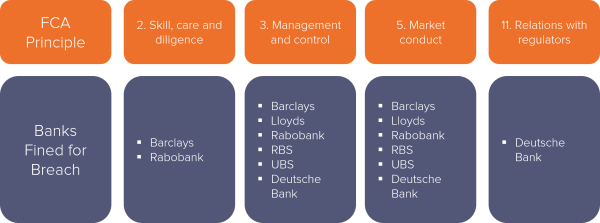

Overview of FCA Principle Breaches

The chart below summarises the breaches of the FCA Principles for Business by various banks as identified in the FCA’s reports on LIBOR manipulation.1 While some principles, such as 3 and 5, were found to have been breached by every bank fined to date, others, such as 2 and 11, were broken only by one or two banks. The full definitions of each principle can be found here.

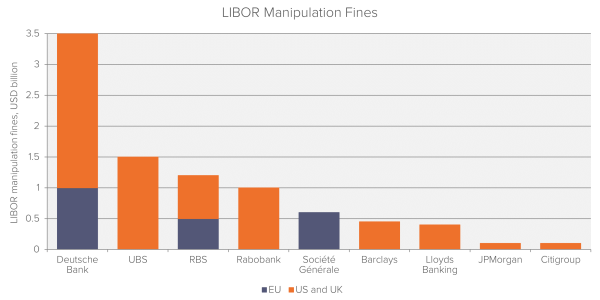

Overview of Fines Imposed

The following chart provides an overview of the fines imposed to date for LIBOR manipulation, broken down between the EU, and the US and UK.2 As can be seen, the fines recently imposed on Deutsche Bank are significantly larger than those imposed on any other bank.

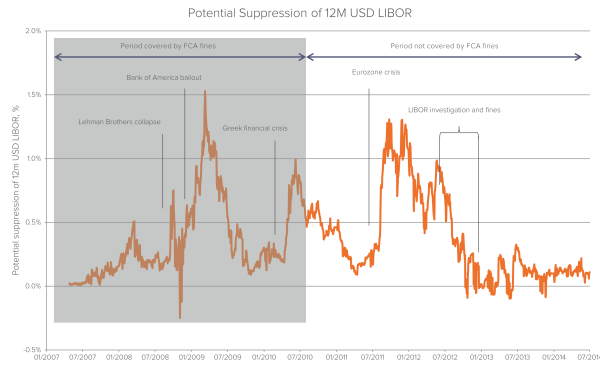

Manipulation Period Covered by FCA Notices

The chart below highlights the period containing the dates identified by the FCA as dates on which LIBOR manipulation took place.3 We also plot the potential suppression of USD LIBOR identified by Fideres’s proprietary statistical models.4 While we touch on this in more detail in the following section, the key point to note here is that the vast majority of the dates identified by the FCA fall before some of the key periods of potential suppression that we have identified, particularly around the Eurozone crisis.

Room for Improvement

While it is, undoubtedly, encouraging to see banks being held accountable for their actions, there are a number of omissions common to the FCA reports that we feel need to be addressed moving forward:

- Lack of suppression findings – Despite the hefty fines imposed by the FCA (and other regulators), the majority of the regulatory findings concerned occasional, day-to-day manipulation driven by the relevant banks’ exposures to the fixing on the given day. In terms of private lawsuits, the likely impact of focusing on sporadic manipulation is small damages, except for the possibility of rescission of impacted transactions. What is lacking is any real focus on the potential suppression of LIBOR that, as highlighted by Fideres’s research, may have been present between 2007 and 2012.5 Such findings would likely lead to significantly higher damages.

- Lack of quantitative analysis used – What was clear from the FCA’s reports was the lack of use of quantitative, data-driven analysis in arriving at their conclusions. While online chats and telephone calls between traders were a fruitful source of information, the crackdown imposed by banks on such communications may reduce the effectiveness of such analysis in future scandals.

- No pointing towards systematic cultural issues – Much of the FCA’s findings were focused on the failure of management to exercise sufficient control to prevent individual traders from engaging in manipulative practices in respect of LIBOR. The systematic cultural issues in the banking industry that have pervaded many of the recent benchmark scandals were not addressed.

Please contact us at research@fideres.com if:

- You would like to discuss any of this information further;

- You have a client portfolio that you believe may have been impacted by the alleged LIBOR manipulation; or

- You would like to discuss specific information on which classes of investors are most likely to have been impacted by the alleged LIBOR manipulation.

Sources

1 FCA LIBOR notices.

2 Financial Times. ‘Deutsche Bank pays record fine for Libor manipulation’. April 23, 2015.

3 FCA LIBOR notices.

4 Bloomberg data, Fideres’s calculations.

5 Pressure from management to keep LIBOR submissions low was touched on in the FCA notices for Barclays, Lloyds and UBS.