Key Points

- In January 2024, the SEC approved Bitcoin and Ethereum ETFs, opening the door to broader crypto investing with a combined market cap now exceeding $60 billion.

- Despite this milestone, crypto ETFs bring their own set of risks. Unlike traditional ETFs, which rely on established authorized participants (APs), these funds depend on liquidity providers (LPs) with lower credit ratings and reserves, raising concerns about potential disruptions to share creation and redemption processes if LPs encounter instability.

- Market concentration is another red flag, with just three LPs controlling over 70% of the crypto ETF market. This dominance not only stifles competition but also raises the risk of price distortions, which could impede the ETF’s ability to accurately reflect the underlying assets’ value.

- Most crypto ETF LPs are linked to proprietary trading firms, raising concerns about market manipulation or front-running, especially given the limited competition and the lack of robust ethics walls in the industry.

- Crypto ETFs’ reliance on a single custodian is a source of additional risk for investors: any major issues, such as a security breach, could have widespread consequences for investors.

- Crypto ETFs may face increased litigation risk if they fail to fully disclose these distinct risks.

Background on Bitcoin Investment Vehicles

Overview

Interest in cryptocurrencies has exploded over the years, attracting a wide range of investors. Yet, many institutional investors have been hamstrung by restrictions preventing direct investments in digital assets. In response, a wave of cryptocurrency-based investment vehicles, primarily private trusts, emerged to offer exposure to the crypto market.

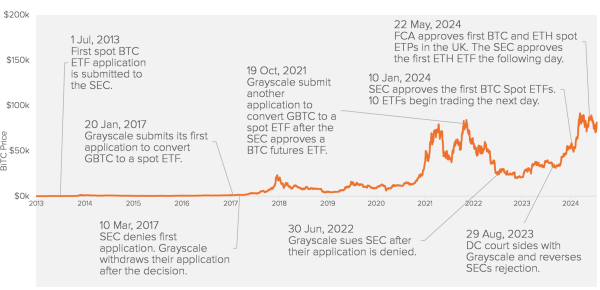

However, these private vehicles lacked the key mechanisms for efficient fund creation and redemption, prompting issuers to file numerous ETF conversion applications with the SEC as early as 2013. For years, the SEC rejected these proposals, citing concerns over market manipulation and investor protection until January 10, 2024, when it adopted rule changes permitting the creation of Bitcoin ETFs on major exchanges.1 The first ten Bitcoin ETFs began trading the following day.2 Subsequently, the SEC approved Ethereum (ETH) spot ETFs on May 23, 2024, after which nine ETH ETFs began trading on July 23, 2024.3

Figure 1 Timeline of Crypto ETFs

As of September 30, 2024, these newly created crypto ETFs had a total market capitalization of over $68bn. In the case of Bitcoin, Blackrock and Grayscale’s ETFs hold roughly 3% of all coins outstanding.

Significant Price Distortions Before ETF Conversions

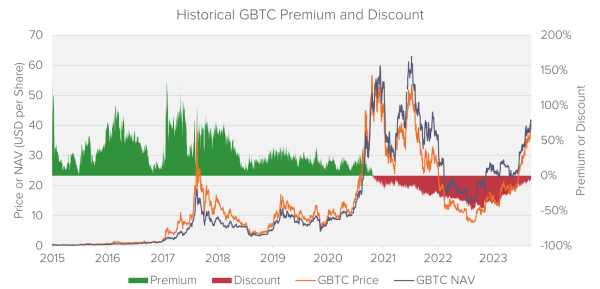

Prior to their transition into publicly traded ETFs, the pain point of private crypto investment vehicles was the significant and persistent disparity between their share price and net asset value (NAV) per share. This discrepancy meant that investors in these vehicles often saw returns that diverged sharply from those of the underlying assets.

Take Grayscale’s Bitcoin Trust (GBTC) as a prime example (Figure 2). As Bitcoin surged to nearly $60,000 in March 2021, GBTC investors endured steep discounts, with the trust trading as much as 50% below its NAV. Not only did investors suffer from the broader decline in Bitcoin’s price, but they were also stuck with the inability to redeem their GBTC shares for actual Bitcoin, further exacerbating their losses.4

This prompted GBTC and other funds to seek ETF conversion, using creation and redemption mechanisms to align NAV with the traded share price.

Figure 2 GBTC Premium and Discount; Source: Bloomberg, Fideres

The Mechanics of ETF Creation and Redemption

Typical ETF Creation and Redemption Structure

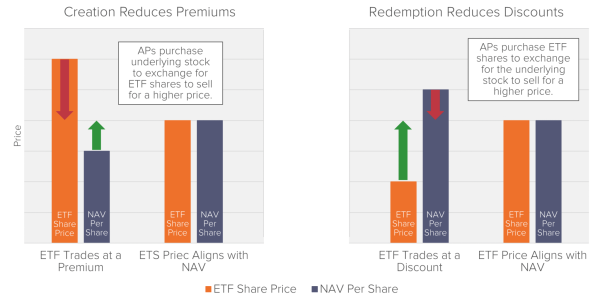

ETFs maintain alignment between their net asset value (NAV) per share and the traded share price through a creation/redemption mechanism, overseen by Authorized Participants (APs), who are typically large financial institutions. APs leverage arbitrage opportunities for risk-free profits, helping keep the ETF’s share price close to its NAV. When the share price falls below NAV, APs buy shares at the lower price, redeem them for underlying assets at NAV, and pocket the difference, pushing the price up. Conversely, when the share price exceeds NAV, APs buy underlying assets, create new shares, and sell them at the higher price, driving the price down. This continuous AP activity is key to maintaining price-NAV alignment (Figure 3).

Figure 3 ETF Creation and Redemption Process

Bitcoin ETFs’ Creation and Redemption Structure

The SEC mandates Bitcoin spot ETFs to use a cash-only creation and redemption process, meaning APs can only exchange cash for shares, not Bitcoin directly. This necessitates fund providers to work with a newly introduced Bitcoin trading counterparty, or Liquidity Provider (LP), to convert between cash and Bitcoin.

While the SEC has not explicitly detailed the rationale behind this requirement, it may aim to reduce risks related to money laundering or prevent self-dealing by market makers. As highlighted in Grayscale’s own presentation to the SEC, many traditional bank APs lack the ability to transact in BTC, giving an advantage to those that can.5

Concerns for Crypto ETFs

Potential for Market Manipulation

Before approving the first spot crypto ETF, the SEC had already approved Bitcoin Futures ETFs, trusting the CME’s surveillance system to curb manipulation risks in the futures market. Spot crypto ETF applicants argued that this system should extend to the spot market, pointing to the strong correlation between Bitcoin futures and spot Bitcoin. However, even in its approval, the SEC did not find or provide quantitative evidence proving that Bitcoin and Bitcoin futures are “functionally identical.”6

The SEC’s analysis, based on a limited number of platforms, instead showed an intraday correlation as low as 67.9%, suggesting significant differences between the futures and spot markets. This implies that some of the possible sources for manipulation identified by the SEC still exist and that CME’s futures market surveillance may not catch all manipulations in spot cryptos. Specifically, the SEC listed the following types of potential spot bitcoin price manipulation:7

- Wash trading: engaging in simultaneous buying and selling of Bitcoin to create a misleading impression of market activity.

- Price manipulation: individuals with dominant positions in the Bitcoin spot market influencing prices.

- Network hacking: unauthorized intrusions into the Bitcoin network or trading platforms.

- Malicious network control: actions aimed at exerting harmful control over the Bitcoin network.

- Insider trading: trading based on material, non-public information, or spreading false and misleading information.

- Stablecoin manipulation: manipulative activities involving purported “stablecoins,” such as Tether (USDT).

- Trading platform fraud: fraud and manipulation occurring on Bitcoin trading platforms.8

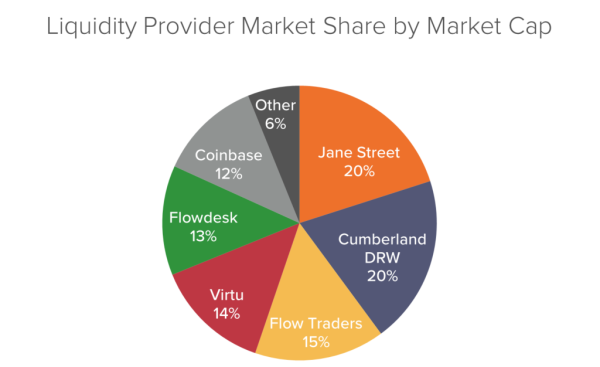

Market Concentration

As detailed above, the stability and tradability of an ETF’s price hinge on the ongoing creation and redemption of fund shares. Simply labeling a fund as an “ETF” does not ensure it will be actively tradable at all times. For this to happen, the fund must actively collaborate with APs and have agreements in place that require APs or other third parties to provide ongoing creation and redemption services, thereby maintaining the ETF’s price stability.

For stock ETFs, this process typically involves a large number of APs, which helps to prevent any single entity from exploiting long-term, risk-free arbitrage opportunities. However, crypto ETFs face distinct restrictions — they are not allowed to trade cryptocurrencies . Like the AP market for stock ETFs, the crypto ETF market similarly needs competition among LPs to ensure accurate price tracking and prevent opportunities for long-term, risk-free gains. Currently, the $68 billion crypto ETF market is characterized by significant concentration among a few LPs, which raises concerns about failure/reduced efficiency in the fund creation/redemption process.

Figure 4 Crypto ETF Liquidity Provider Market Share as of Q2 2024; Source: SEC, Fideres

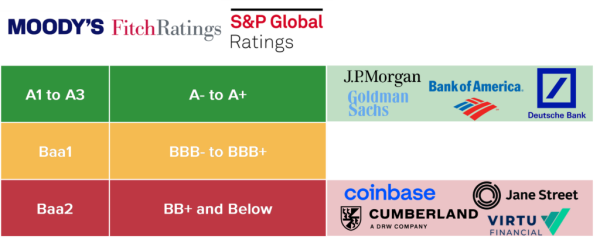

Credit Risk

These LPs also play a significant role as market makers in the cryptocurrency space. Unlike heavily regulated traditional bank APs, these trading firms carry elevated credit risk (Figure 5). This is due to their primary focus on the highly volatile crypto market and their relatively smaller capital reserves which may not be enough to mitigate the impact of extreme events like the situation witnessed in FTX’s bankruptcy. Consequently, investors in crypto ETFs are likely to see higher average premiums or discounts compared to traditional equity ETFs.

Figure 5 AP/LP Long-term Credit Ratings

Many of these entities also face legal actions and government investigations for issues like selling unregistered securities,9 receiving preferential treatment on exchanges10, and engaging in market manipulation.11 Without compelling evidence showing that these new crypto ETF LPs have implemented a robust ethics wall for their newly created roles in the ETF market, the probability of misconduct, such as market manipulation or frontrunning, may be notably higher compared to traditional stock ETFs.

Market Manipulation Risk

The substantial trading volume driven by crypto ETFs also grants these LPs access to a considerable amount of trading data. This information is highly valuable, as significant creation or redemption activity in crypto ETFs can impact the prices of the underlying cryptocurrencies, and trading on such confidential insider information can lead to significant profits.

Without robust information barriers, LPs or their affiliated entities might be tempted to breach federal securities laws, leading to potential legal actions from ETF or crypto investors (for example, under Section 10(b) of the Exchange Act and rule 10b-5 thereunder).

Similar violations recently led to Morgan Stanley being fined over $249 million for leaking and misusing confidential block trade information.12

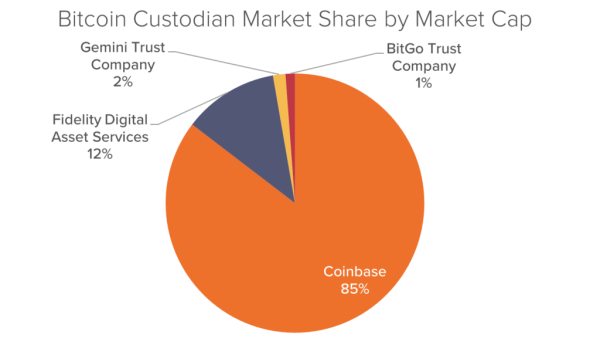

Custodians Concentration Risk

Finally, Crypto ETFs rely on non-traditional custodians to safeguard their assets. As of 2024 Q2, Coinbase held 85% of all Bitcoins owned by Bitcoin ETFs. This heavy concentration is concerning, particularly given historical precedents like the Mt. Gox security breach in 2014, where the world’s largest Bitcoin exchange lost approximately 850,000 Bitcoins. If Coinbase were to encounter major operational issues, security breaches, or insolvency, the fallout for crypto ETFs and their investors could be disastrous. This dependence on a single custodian amplifies these vulnerabilities and underscores the potential risks involved.

Figure 6 Crypto ETF Custodian Market Share as of Q2 2024; Source: SEC, Fideres

Conclusions

In summary, the SEC’s approval of crypto ETFs was predicated on the assumption that the CME’s surveillance system for futures would also address manipulation risks in the spot market. However, the SEC’s own findings instead reveal significant disparities between these markets, suggesting that manipulation risks—such as wash trading and price manipulation—can persist unnoticed in the spot market.

While ETF price stability relies on the efficient creation and redemption of shares, crypto ETFs face distinct challenges due to their dependence on LPs with lower creditworthiness and higher market concentration compared to traditional APs.

The heavy reliance on a single custodian, like Coinbase, further compounds these risks, as any major issue could have severe repercussions for both the ETFs and their investors.

As a result, spot crypto ETFs may face heightened litigation risks if they fail to adequately disclose these distinct risks, and investors suffer losses from market manipulation or failures in the fund creation and redemption process.

Sources

1 https://www.sec.gov/files/rules/sro/nysearca/2024/34-99306.pdf

2 Including, the Grayscale Bitcoin Trust, the Bitwise Bitcoin ETF, the iShares Bitcoin Trust, the Valkyrie Bitcoin Fund, the ARK 21Shares Bitcoin ETF, the Invesco Galaxy Bitcoin ETF, the VanEck Bitcoin Trust, the WisdomTree Bitcoin Fund, the Fidelity Wise Origin Bitcoin Fund and the Franklin Bitcoin ETF. The Hashdex Bitcoin ETF did not receive approval until March 2024.

3 Including, the Grayscale Ethereum Trust, the Grayscale Ethereum Mini Trust, the Franklin Ethereum Trust, the VanEck Ethereum Trust, the Bitwise Ethereum ETF, the 21Shares Core Ethereum ETF, the Fidelity Ethereum Fund, the iShares Ethereum Trust, and the Invesco Galaxy Ethereum ETF.

4 See e.g., “Transfer Restrictions” section of GBTC’s 2022 Form 10-K.

5 https://www.sec.gov/comments/sr-nysearca-2021-90/srnysearca202190-318679-829963.pdf; Moreover, SEC’s Staff Accounting Bulletin No. 121 (“SAB 121”) also mandates publicly traded banks to put crypto they custody on balance sheets, contrary to how traditional securities are treated. This affects capital, liquidity and other requirements and effectively precludes banks from being able to custody these assets without affecting their other lines of business. See https://www.sec.gov/regulation/staff-interpretations/accounting-bulletins/old/staff-accounting-bulletin-121.

6 Despite the approval, the SEC chair Gary Gensler cautioned the market that “bitcoin is primarily a speculative, volatile asset that’s also used for illicit activity including ransomware, money laundering, sanction evasion, and terrorist financing.” See https://www.sec.gov/news/statement/gensler-statement-spot-bitcoin-011023

7 See, for example, https://www.sec.gov/files/rules/sro/nysearca/2022/34-94999.pdf

8 See, for example, Griffin, John M., and Amin Shams. “Is Bitcoin really untethered?.” The Journal of Finance 75.4 (2020): 1913-1964.