Key Points

Global ETF Landscape

An exchange-traded fund, or ETF, is a pooled investment vehicle listed and traded on a stock exchange. ETFs offer many benefits to investors, including low-cost diversification and tax efficiencies. As a result, the market for ETFs has grown significantly in the past decade, with a compound annual growth rate (CAGR) of over 25%, compared to 6% CAGR for mutual funds.

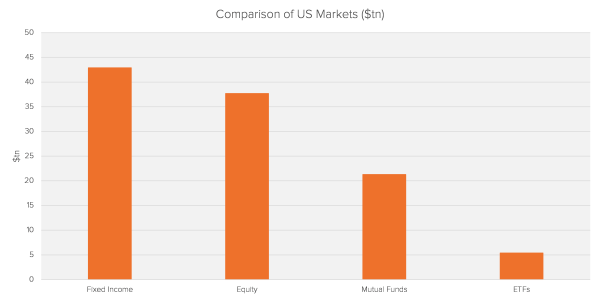

As of 2019, ETFs controlled $5.4tn in Assets Under Management (AUM) globally, with the US accounting for just over 70%. Though only a fraction of other more liquid markets, the ETF market is growing at a much faster rate. Bank of America estimates that ETF AUM will reach $50tn by 2030, which is the combined size of US equity and mutual funds markets today.

Structure of ETFs

ETF Creation and Redemption Process

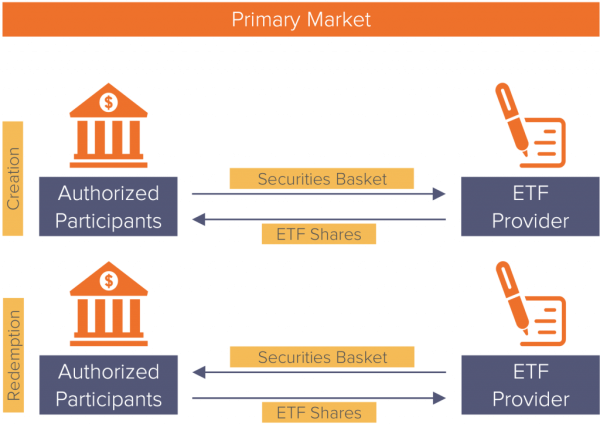

A unique feature of ETFs is the creation/redemption mechanism which keeps secondary market prices in line with the Net Asset Value (NAV) of its underlying securities. The key players in this process are Authorized Participants (APs) – large financial institutions which transact directly with ETF managers in the primary market, and trade with investors in the secondary market.

APs purchase shares from the ETF in large blocks called creation units (typically between 25,000 and 200,000 shares), in exchange for a basket of securities (called the creation basket). APs can then sell all or part of the shares to investors on the secondary market, increasing the supply of ETF shares and influencing its price. Conversely, APs can buy shares from investors and redeem them in exchange for a basket of securities from the ETF.

The creation/redemption process is driven by the APs’ pursuit of risk-free profits. If the ETF share price drops significantly below NAV, APs will buy shares on the secondary market at the low price and redeem them in exchange for a basket of securities with a value equal to NAV, pocketing the difference. This arbitrage opportunity incentivizes APs to buy investor shares, until the price is close or equal to NAV and arbitrage is no longer possible. Conversely, if ETF shares are trading at a premium to NAV, APs can purchase a basket of securities, convert them to ETF shares at NAV, and sell these shares for the higher price on the secondary market.

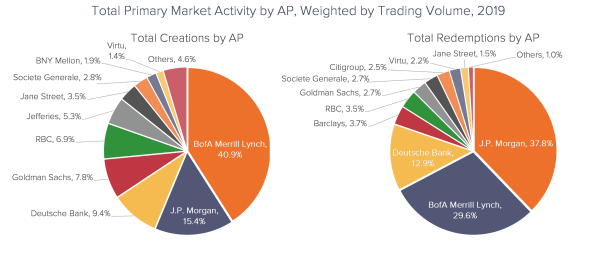

AP Activity in the Primary Market for US ETFs

We find that only a handful of APs are actively redeeming or creating shares each year. In addition, our analysis indicates that the primary market is highly concentrated – the top three APs accounted for over 65% of all creations and 80% of all redemptions in 2019.

Source: SEC, Fideres’s Analysis

ETF Inefficiencies

The AP arbitrage mechanism should provide sufficient incentives for APs to actively correct the price/NAV discrepancies in the ETF market. Competition among APs should eliminate any opportunity for risk-free gains. However, this is not what we consistently observe in the market. This issue became especially acute during the COVID-19 pandemic, when even the most liquid ETFs started trading at upwards of 6% discount to NAV.

In most cases, these record discounts persisted for more than a week despite large redemption efforts by APs. Large and persistent differences between ETF prices and its NAV are characterized by researchers as an ETF inefficiency. Scholars have found that inefficiencies persist even when accounting for the illiquidity of underlying assets, and have flagged the fact that APs face a conflict of interest between their roles as ETF arbitrageurs and as bond dealers.

Potential Competition Issues in the ETF Primary Market

While the existing literature identifies several reasons behind ETF inefficiencies, competition issues in this market have not been systematically investigated. We believe that the ETF primary market may be vulnerable to manipulation and anti-competitive practices due to high concentration, conflicts of interest, and potential barriers to entry. More transparency in the form of primary market transactional data could increase public trust in ETFs and allow researchers to examine competition issues directly.

| Number of funds | AS | TE | R-Squared | Management fee starting | Fund size (EUR) | |

|---|---|---|---|---|---|---|

| Sub-sample | 1,014 | 71.24% | 4.68% | 91.33% | 1.49% | 586,232,604 |

| Classification 1 | 166 | 43.25% | 2.80% | 96.49% | 1.48% | 400,119,115 |

| Classification 2 | 67 | 35.95% | 2.12% | 98.14% | 1.46% | 272,966,085 |

| Classification 3 | 63 | 35.69% | 2.05% | 98.33% | 1.47% | 272,153,044 |