Research

Jingle Bills, Jingle Bills, Jingle All The Way

Key Points Fideres’s original investigation uncovers widespread discriminatory conduct in the market for household gas/electricity – affect...

CDOR is a benchmark index for bankers’ acceptances with 1-, 2-, 3-, 6-, or 12-month maturity bands. It is determined daily from a survey of the bid prices of seven market makers in bankers’ acceptances. For each maturity band, the index is calculated as the arithmetic average after the high and low bid rates are excluded.

According to one widely-cited estimate,1 CDOR was used in 2014 to determine interest payments on:

During the financial crisis and its aftermath, CDOR submitting panelists had largely the same incentives to suppress the rates they reported as the incentives which were documented in the global LIBOR manipulation cases of 2012. If LIBOR represents the rate at which banks expect to borrow, CDOR represents the rate at which they are willing to lend. A lower lending rate indicates a lower cost of borrowing for banks and so there was an incentive for CDOR submitters to potentially under-report their lending rates during the crisis in order to falsely signal higher creditworthiness.

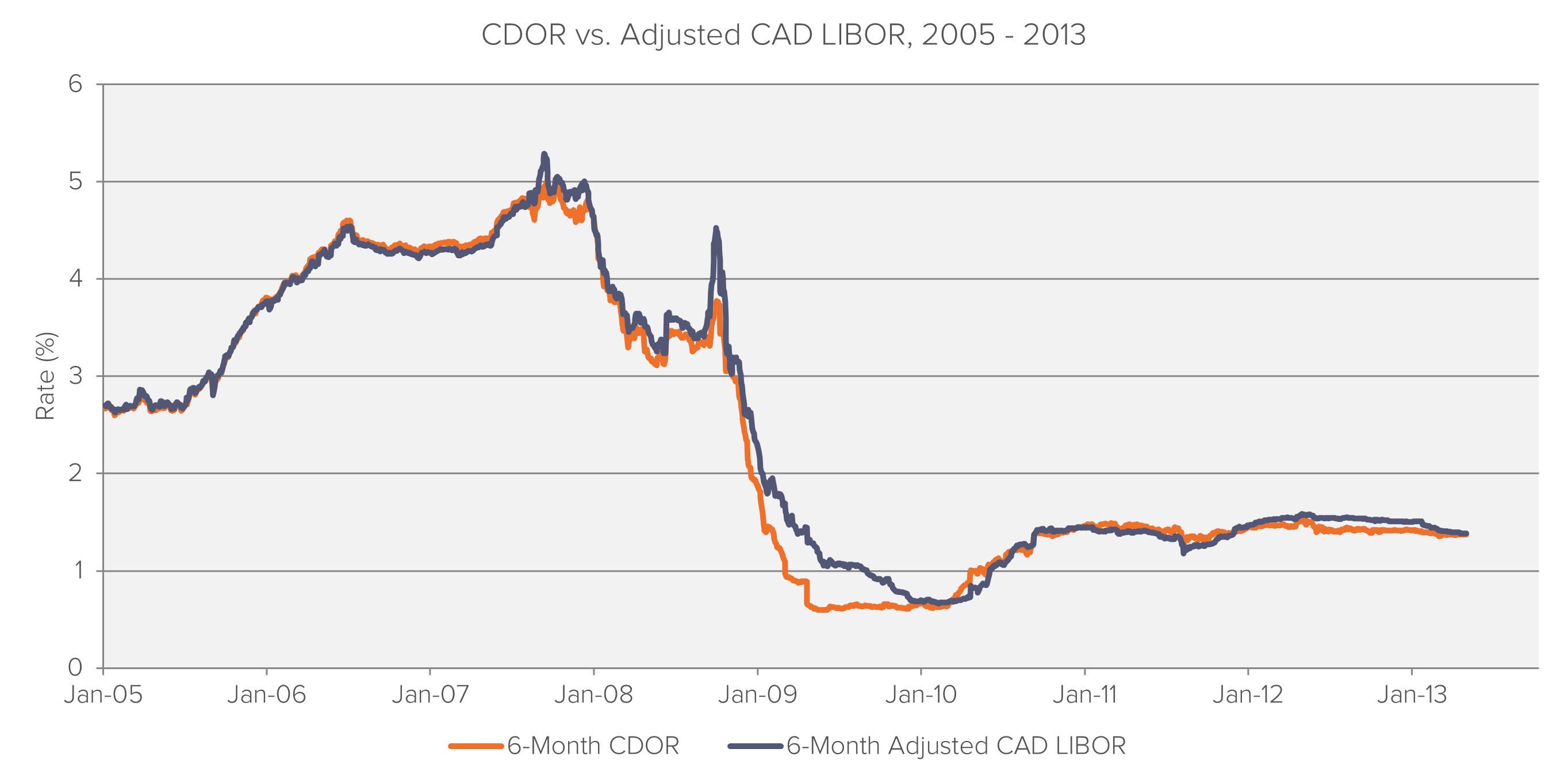

The chart below shows that under normal conditions, CDOR slightly exceeded CAD LIBOR, adjusted to account for potential differences in credit quality of submitting banks. The sudden divergence between CAD LIBOR and CDOR that emerges between September 2007 and September 2009 hints that banks may have been understating the rate at which they could profitably lend.

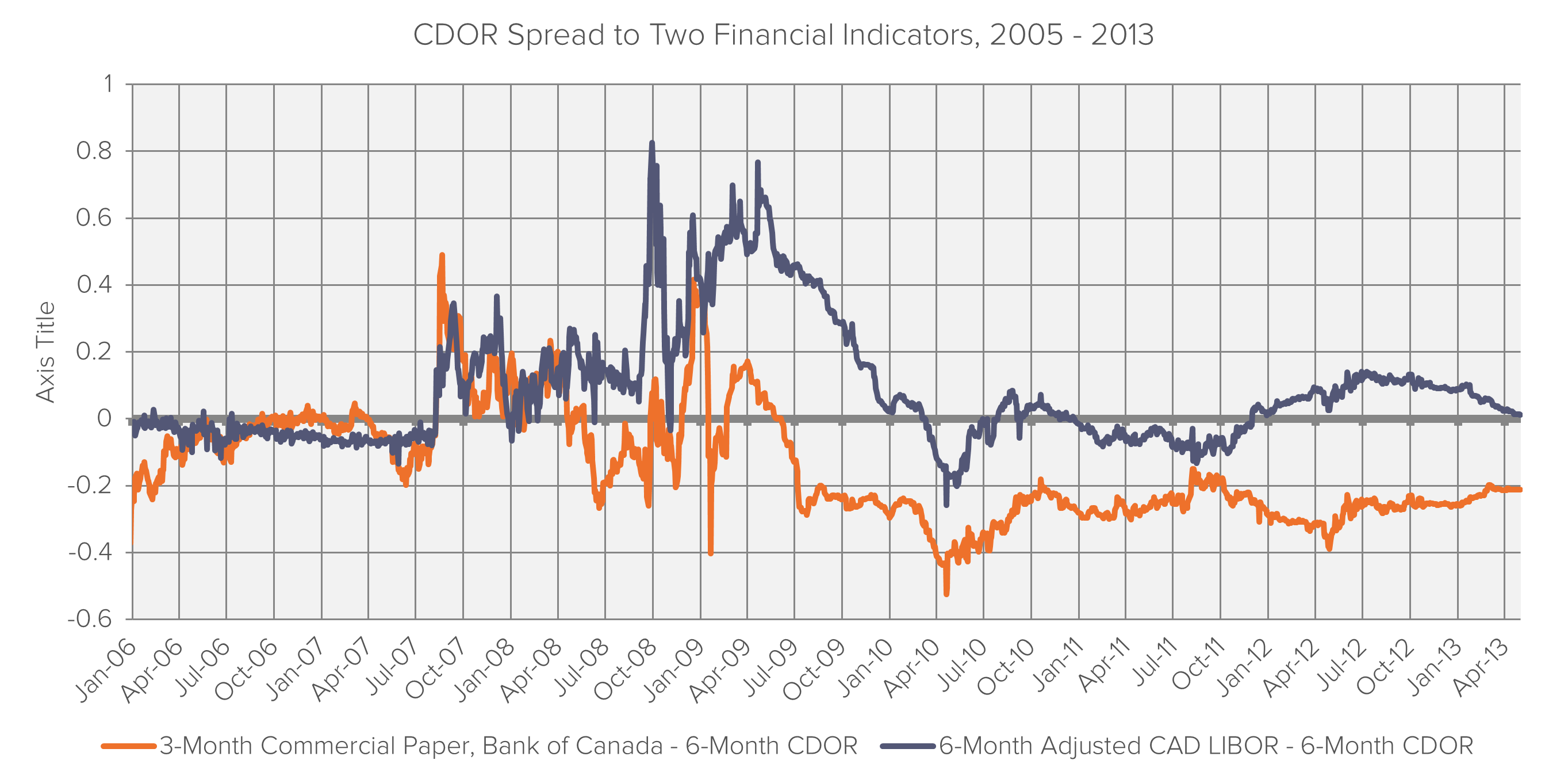

Like CAD LIBOR, Prime Commercial Paper rates should closely track CDOR. During the crisis, a spread between CDOR and the Commercial Paper rate emerges of the same overall magnitude as the spread between CAD LIBOR and CDOR. Both spikes in the graph below occur during the same period of abnormally low CDOR submissions. The close link between the Commercial Paper rate and CAD LIBOR supports the suspicion that the lower CDOR rate was potentially set too low.

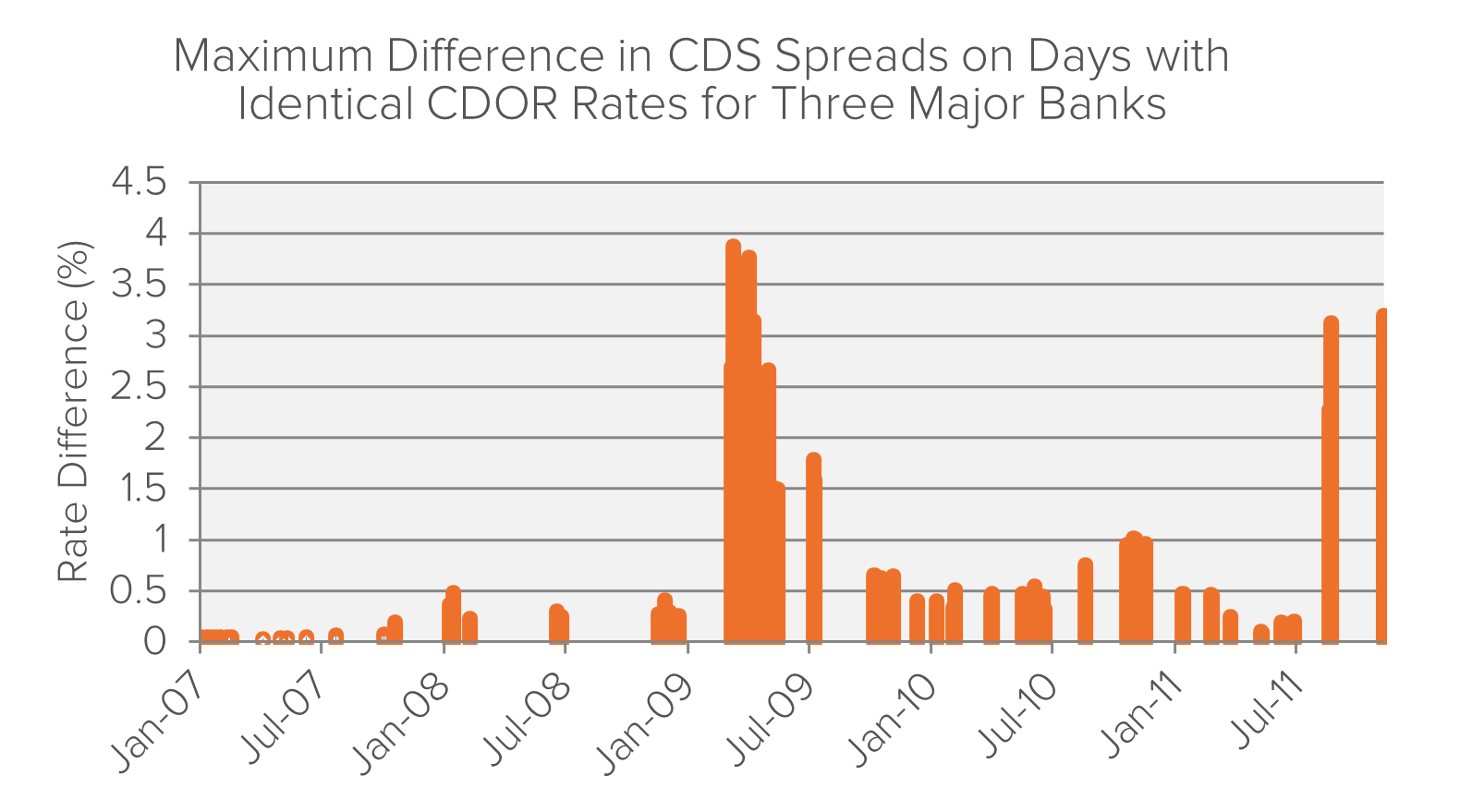

During the height of the financial crisis, 12-month CDS spreads of three large international banks diverged by as much as 50 to 400 basis points, even on days when all three banks submitted identical CDOR rates. Had the banks been offering rates honestly, wide differences in CDS spreads should have implied some difference in CDOR submissions.

The graph below charts the maximum CDS spread difference for the major banks on days when they submitted the same CDOR rate. In the absence of manipulation, we would expect to see very little difference. In practice, there appear to be large differences, particularly during the financial crisis. Effect of Rate-Fixing Scandals

Effect of Rate-Fixing Scandals

In August 2011, as the LIBOR scandal unfolded, the IIROC announced a formal investigation into the CDOR rates submission process. For the period around the announcement, the reported CDOR remains more or less steady in the lower tenors. However, at some point in late 2011, the dispersion of the submissions spiked as one of the banks began to submit substantially higher rates than other banks. Soon after the IIROC published its findings in January 2013, this bank’s submissions returned to conformity with the average rate. This episode may imply that the bank in question reverted to non-collusive submissions in response to the investigation, with the higher rate they posted in this period indicating the correct CDOR rate.

Max joined Fideres in 2016. He has led the development and implementation of economic models for major collective actions in the US and the UK, contributing to litigation on a variety of topics. His reports and econometric work has been included in cases for conduct including, among others, the FX and LIBOR benchmark manipulation, digital market monopolisation by Apple and Amazon, and consumer claims against a cartel of US generic drug manufacturers, abuse of market power by large regional US hospital systems, restriction of the right to repair by John Deere, and the combined abuse of dominance by Visa and Mastercard in UK payment systems. Before joining Fideres, Max worked at the national laboratory in Los Alamos, New Mexico, as part of a team designing neural networks for applications in machine learning. Max holds an MSc in Economic History from the London School of Economics.

Key Points Fideres’s original investigation uncovers widespread discriminatory conduct in the market for household gas/electricity – affect...

Damage estimation in data breach litigation.

The use of active share in identifying closet index funds.

London: +44 20 3397 5160

New York: +1 646 992 8510

Rome: +39 06 8587 0405

Frankfurt: +49 61 7491 63000

Johannesburg: +27 11 568 9611

Madrid: +34 919 494 330