Research

Structured Credit Ratings

Still navigating in troubled waters?

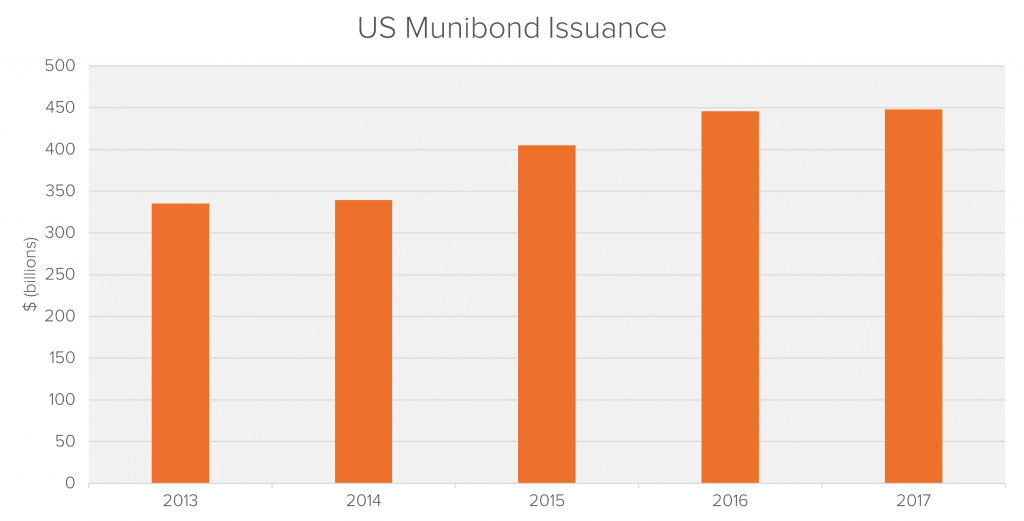

Outstanding Muni Bond debt in the United States numbers in the trillions of dollars ($3.8tn as of Q3 2017). The average daily trading volume of Muni Bonds between 2007 and 2017 was approximately $9bn. The chart below shows the volume of new Muni Bond issuance for the past five years.

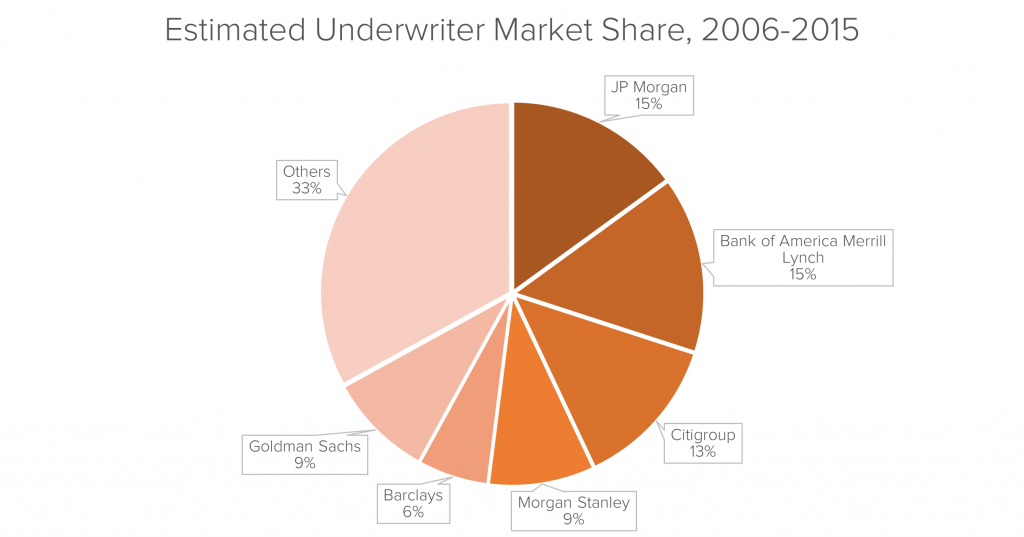

Unlike similar securities (such as US Treasuries), Muni Bonds are not priced in a competitive bidding process. Municipalities typically ‘outsource’ the pricing of their bonds to underwriters, who generally come from a small group of large banks. The chart below estimates underwriters’ market share, based on a sample of trade and issuance data for Muni Bonds provided by Bloomberg:

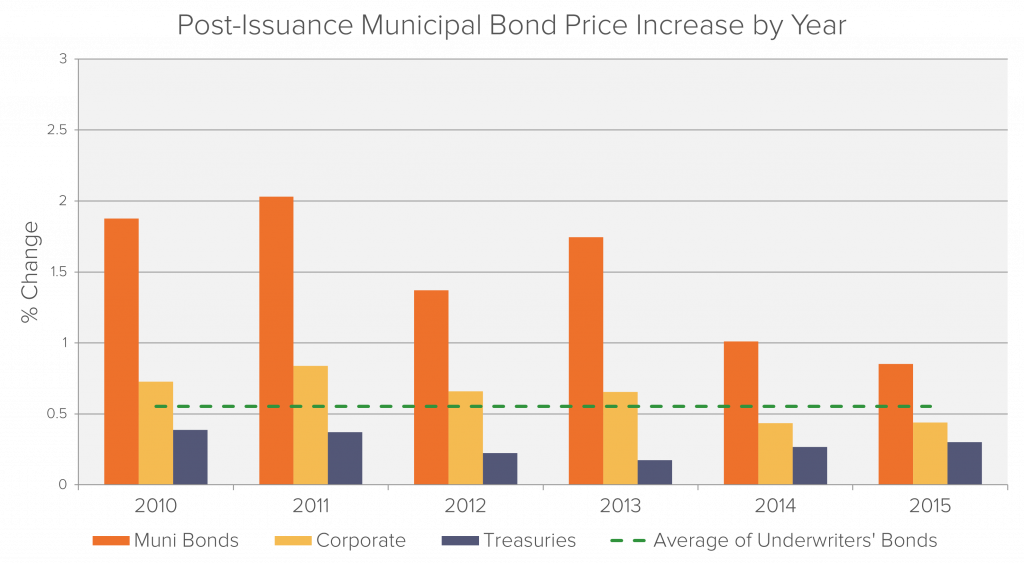

Issuers will typically price their bonds generously to attract investors, so it is normal for the price of newly listed securities to rise in the secondary market after they begin trading. Nevertheless, Fideres’s findings show that the price of Muni Bonds increases far more than securities in similar markets.

We analysed a Bloomberg sample of price increases for Muni Bonds, issued between 2006 and 2015, and compared them to US corporate bonds and US Treasury bonds.1 The results are shown in the charts below:

Weighted by issuance size, the average Muni Bond price increase is 163 bps, compared to 55bps for underwriters’ bonds, 33bps for Treasuries, and 64bps for corporates. This implies that there is sufficient market demand for municipalities to issue bonds at lower yields, and save significantly on borrowing costs. Underwriters are also much better at pricing their own bonds than Muni Bonds.

While the numbers in the chart represent national averages, these conceal glaring individual cases of mispricing. Fideres has identified states whose Muni Bonds increase in price by up to 12% on their first day of trading.

Before a Muni Bond is issued, underwriters are tasked with researching demand for the bond and pitching it to prospective investors. They then give the issuer feedback and agree final terms for the bond’s price. The underwriters also allocate the initial issuance to investors and typically retain a portion, in order to provide secondary market support. When the bonds are issued, investors pay cash to the issuer and receive the bonds, after which they trade in the secondary market.

Several reasons may explain the systematic mispricing of Muni Bonds:

Fideres’s research raises important questions regarding the pricing of Muni Bonds:

In the light of this evidence, particularly given its implications for taxpayers, it is surprising that very few issuers have taken action to improve the pricing of their own securities.

1 The sample is restricted to non-taxable, fixed coupon bonds, with notional sizes of $50m or greater.

Max joined Fideres in 2016. He has led the development and implementation of economic models for major collective actions in the US and the UK, contributing to litigation on a variety of topics. His reports and econometric work has been included in cases for conduct including, among others, the FX and LIBOR benchmark manipulation, digital market monopolisation by Apple and Amazon, and consumer claims against a cartel of US generic drug manufacturers, abuse of market power by large regional US hospital systems, restriction of the right to repair by John Deere, and the combined abuse of dominance by Visa and Mastercard in UK payment systems. Before joining Fideres, Max worked at the national laboratory in Los Alamos, New Mexico, as part of a team designing neural networks for applications in machine learning. Max holds an MSc in Economic History from the London School of Economics.

Still navigating in troubled waters?

As GDPR takes off, UK litigators may become frequent filers.

Are UK Water Companies Breaching Competition Law?

London: +44 20 3397 5160

New York: +1 646 992 8510

Rome: +39 06 8587 0405

Frankfurt: +49 61 7491 63000

Johannesburg: +27 11 568 9611

Madrid: +34 919 494 330