Key Findings

Fideres has conducted a preliminary investigation into UK mobile network operators. This follows the four largest UK mobile network operators – EE/BT, O2, Vodafone and Three – concurrently raising prices to their pay monthly fixed term contracts. We have found that:

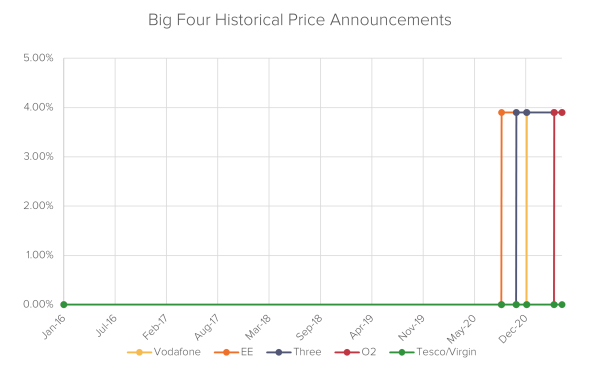

- The ‘Big Four’ mobile network operators announced identical price increases within a space of four months from each other.

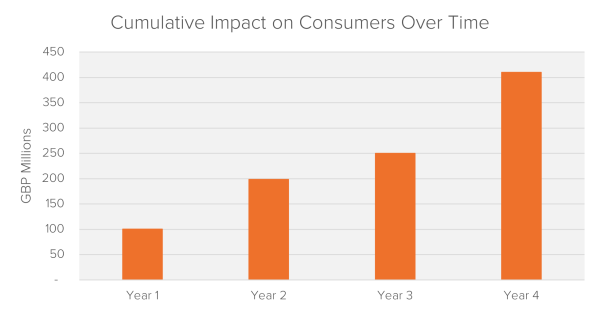

- Price increases of 4.5% in April 2021 will lead to additional consumer spending of almost £400m a year.

- Collectively, the Big Four have a market share of approximately 87% in the UK.

- The merger between O2 and Virgin Mobile, recently approved by the CMA, will lead to further market concentration and more harm to consumers.

Parallel Price Increases

In October 2020, EE and BT Mobile (which jointly have a 28% market share according to BT’s 2018 annual report1 announced that any new fixed term pay monthly contract would have a provision for the automatic increase of contract prices on the 1 April each year. The rate of increase is specified to be RPI +3.9%. Based on the March RPI index, this translates into a price increase of 4.5%. Plusnet, also owned by BT, has implemented an identical price increase as of October 2020.

O2 and Vodafone, representing 26% and 21% of the market, respectively, followed suit and introduced identical provisions. Three, with a market share of 12%, introduced the same rate of increase, but instead of referencing the inflation index, they specified it to be equal to 4.5%, also to kick-in on 1 April (incidentally, 4.5% is equal to RPI +3.9% for this year).

Source: Companies’s Websites

It does not appear that these contract changes have also been imposed on customers with older contracts.

Together, the top four mobile operators represent over 87% of the market. Two smaller operators – Virgin Mobile and Tesco Mobile – did not introduce similar amendments to their contracts. Virgin Mobile maintained a price increase equal to RPI, while Tesco Mobile continues to maintain constant prices throughout the term of the contracts.

Price increases of this magnitude have not been introduced in other European markets. Our research shows that annual contract price increases in the EU/EEA are typically aligned with the respective national inflation index. Mobile phone price hikes above the rate of inflation are a UK anomaly.

Background on Fixed-Term Mobile Contracts

The UK Landscape of Mobile Network Operators

In the UK, there are two types of mobile phone service providers:

- Mobile Network Operators (“MNOs”) – these are the four largest companies (EE, O2, Vodafone and Three), each operating their own network infrastructure, with similar network coverage across the country.

- Mobile Virtual Network Operators (“MVNOs”) – these are smaller operators, such as BT Mobile, Sky, Virgin Mobile, Tesco Mobile and PlusNet. They rent capacity on the Big Four’s networks in order to operate their services. For example, Tesco Mobile has an agreement with O2, while Virgin Mobile uses Vodafone’s network and BT Mobile and Plusnet rely on EE’s network.

MVNOs tend to offer a more narrow range of services compared to MNOs. MVNOs tend to compete on basic mobile packages such as sim-only plans but may not be a pure competitor to MNOs when it comes to the market for full-service plans. A 2015 Ofcom Strategic Review of Digital Communications Study mentions differences in services used by MVNO customers compared to MNOs2.

Consolidation History of Mobile Networks

EE was borne out of the merger between T-mobile and Orange in 2009. The CMA approved the acquisition of EE by BT in January 2016. In the same year, the European Commission (EC) blocked a proposed merger between O2 and Three. In May 2020, the EU General Court annulled the EC’s decision to block the merger3, finding that the relevant standard of proof of the impact of the proposed merger relating to prices and quality was not met. The EC has appealed this decision to the European Court of Justice. On 14 April 2021, the CMA provisionally cleared the merger of Virgin and O24 and on 20 May 2021, the CMA gave the green light for the merger to take place5. Following the merger, it will be interesting to observe whether Virgin Mobile will maintain price increases at RPI, or align the price increases with O2.

High Competition and Policies Have Historically Contributed to Competitive Consumer Prices

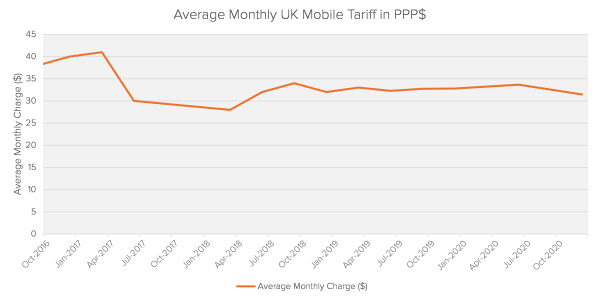

Competition and pro-competitive policies such as the EU ban on roaming charges6 have led to a compression on profit margins for mobile network operators for the past 20 years. Since 2016, prices for mobile services in the UK have been relatively stable.

Source: Point Topic

The Big Four have motivated the parallel price increases with the large investment required to roll out 5G technology across the UK. Given that Vodafone and Three operate networks across several EU countries, if the motivation for the price increases is the cost of 5G implementation, why have they not announced similar price increases in other markets? The answer most likely lies in the relatively higher level of competition in EU markets compared to the UK. The pro-consumer stance of the ECJ, in relation to contract law, could also make unilateral, mid-contract price increases harder to implement.

Fixed Term Mobile Contracts in the UK

Approximately 50% of all pay monthly contracts have an initial fixed term of 24 months, while the remainder of the contracts are approximately equally split between 12 months and 1 month rolling terms.

Until October 2020, all contracts had a maximum annual increase equal to RPI/CPI. It is only then that mid-contract price hikes are introduced.

Regardless of the initial term of the contract, Ofcom data shows that a large proportion of customers do not switch contracts at the end of the initial term. Ofcom’s annual Switching Tracker for 2020 highlighted that 39% of the consumers with a mobile phone contract never switched providers7.

Impact of Price Changes

The identical terms proposed by all major networks could generate a reduction in competition through a stabilization of market share: if all MNOs increase prices at the same time every year, there will be less incentive for consumers to shop around. It remains to be seen, but if MNOs also increase the initial price of the plans in line with the RPI +3.9% stipulated in the contract, switching provider will no longer protect consumers from the “loyalty penalty”.

Following a consultation, in 2013 Ofcom ruled that, as long as price increase clauses are clear and transparent, they are legal and do not give rise to an optional termination for consumers. This is radically different from the stance taken by other regulatory agencies:

- In Germany, consumers have the right to terminate the agreement if the price increase is fractionally above the increase of the general cost of living.

- Canada de facto does not allow clauses allowing telecom operators to unilaterally increase prices without consumers’ consent.

- In Italy, future price increases tend not to be formally documented in the contracts and consumers are entitled to terminate contracts without termination fees, if mobile networks decide to increase tariffs during the life of the contract. Italy and Germany have the lowest prices in Europe for mobile phone contracts.

In a December 2018 report, the CMA highlighted the impact of loyalty penalties, where companies penalize customers who stay on their contracts for the long-term compared to customers who switch. The impact of these latest mobile contract price changes seem to be a reverse of the loyalty penalty, and instead can be thought of as a switchers penalty. Not only will a growing number of consumers (up to 40% of consumer switch contracts) be affected over the coming years, but the significant change in contractual price increases will complicate consumers’ decision making process.

If, as we expect, the Big Four’s contract changes lead to reduced price competition, consumers with expired contracts will be better off remaining on their old plans instead of new offers. The 3.9% increase above inflation imposed by the new contracts will quickly erode any potential savings offered by the new plans. Giving up an old contract, where price increases are capped at RPI or CPI, could be very costly to consumers.

The chart below illustrates Fideres’s projected impact on UK consumers of the contract changes introduced.

Source: Fideres Calculations, Ofcom

This raises a number of questions:

- What obligations do mobile operators have to inform consumers of long term price projections?

- Should Ofcom consider imposing similar conditions on mobile operators as Ofgem imposed on utility companies, whereby utilities are forced to move customers to their cheapest available standard tariff once fixed term contracts expire?

Fideres’s Analysis

When taken as a whole, the evidence gathered might be indicative of anti-competitive conduct on the part of the four largest mobile network operators in the UK.

- The compression of profit margins over the past 10 years is a significant factor and motive for mobile networks to enact anti-competitive measures.

- The timing of the price increases coincides with Brexit. The vacuum created by the lack of jurisdiction of the European Courts in the UK, post-Brexit, combined with Ofcom’s unique stance in Europe in relation to mid-contract price increases, may have provided the UK MNOs with enough incentive for the price increases.

- The UK consumer law regime presents unique features that allows operators to implement unilateral contract changes with little opportunity for consumers to exercise competitive pressure.

- The price increases are identical in quantum and have been introduced in a staggered manner, within a short time frame of three months. This is very common in cases of tacit or explicit collusion.

- The fact that the two largest MVNO players, Tesco Mobile and Virgin Mobile (respectively using O2 and EE/Vodafone’s networks) have not increased prices, excludes the possibility that price increases are driven by increased upstream network costs.

Call to Action

Fideres has filed a complaint with Ofcom and the CMA to take rapid action to investigate mobile network operators’ conduct. As the economy recovers from the COVID-19 slump, it is crucial that competition in the mobile network sector is retained to maintain the UK economy competitiveness against Europe and other major economies.